The Core of Economics: Scarcity and Choice

Economics is fundamentally the study of how society manages its scarce resources to satisfy unlimited human wants. It breaks down into three key foundational realities:

- Unlimited Human Wants: Human desires are endless. As soon as one want is satisfied (e.g., getting a bicycle), a new want arises (e.g., wanting a motorbike).

- Scarcity of Resources: The resources needed to satisfy these wants—such as land, money, raw materials, and time—are limited or finite in supply.

- The Problem of Choice: Because we cannot have everything we want, we are forced to make choices. Choosing one option means letting go of another.

What is Opportunity Cost?

Every time a choice is made, an Opportunity Cost is incurred. It is defined as the value of the next best alternative that you give up to get what you want.

- Example: If you have ₹100 and you choose to buy a textbook instead of a movie ticket, the movie ticket (and the enjoyment it would have given) is the opportunity cost of buying the textbook.

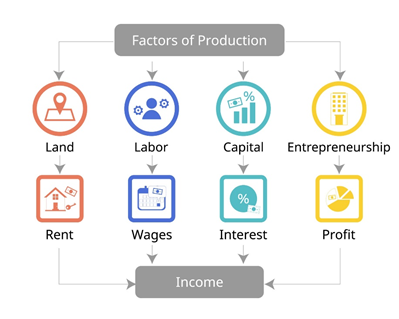

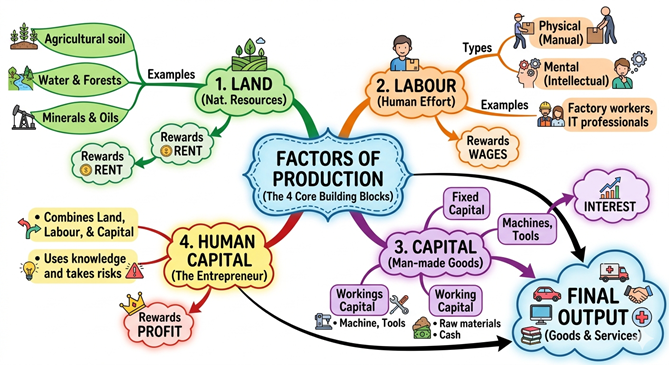

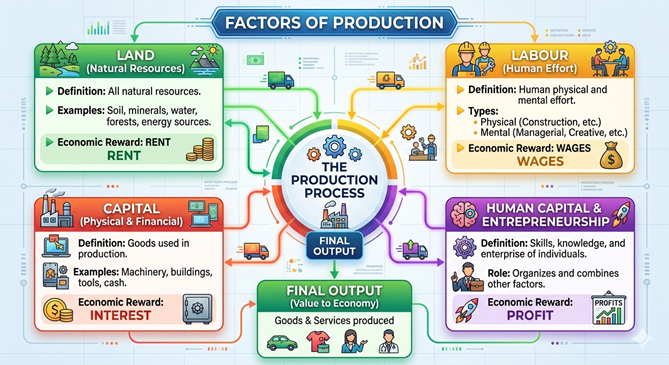

Factors of Production (The Core Building Blocks)

To produce any commodity or service, an economy requires four essential pillars, known as the Factors of Production. Production is impossible if any one of these is missing.

1. Land (Natural Resources)

- Explanation: This includes not just the physical soil or plot of ground, but all natural resources provided by nature for free.

- Examples: Water bodies (rivers, lakes), forests, mineral deposits (coal, iron ore), and agricultural soil.

2. Labour (Human Effort)

- Explanation: The physical or mental effort exerted by humans to convert inputs into finished goods or services.

- Classification:

- Physical Labour: Manual work like a construction worker lifting bricks or a farmer tilling soil.

- Mental Labour: Intellectual work like a software engineer writing code or a manager planning a business strategy.

3. Physical Capital (Man-Made Inputs)

- Explanation: The variety of man-made inputs required at various stages of production.

- Division:

1. Fixed Capital: Tools, machines, computers, and buildings. They are called “fixed” because they can be reused over many years and do not disappear after a single production cycle.

2. Working Capital: Raw materials and cash in hand. They are called “working” because they are consumed or used up completely during a single cycle of production (e.g., yarn used by a weaver, or money used to pay daily wages).

4. Human Capital (Enterprise)

- Explanation: The knowledge, expertise, skills, and risk-taking ability needed to put together land, labour, and physical capital to produce a meaningful output. Without human enterprise, the other three factors remain idle.

3. Types of Economic Activities

Human activities are broadly classified into two categories based on their primary economic objective:

Market Activities

- Definition: Activities performed with the objective of earning money, wages, remuneration, or profit.

- Key Characteristic: The goods or services produced are sold directly in the market.

- Examples: A doctor treating patients in a private clinic, a factory worker producing shoes for a salary, or a shopkeeper selling groceries.

Non-Market Activities

- Definition: Activities performed primarily for self-consumption or out of love, care, and duty.

- Key Characteristic: No income or profit is generated from these actions, and they do not enter the commercial market.

- Examples: A mother cooking food for her family, a hobbyist growing vegetables in their backyard for personal meals, or cleaning your own house.

4. Sectors of the Economy

Every economy organizes its production into three interconnected sectors based on the nature of the economic activity:

Sector | Nature of Activity | Real-Life Examples |

Primary Sector | Directly exploits natural resources to produce raw items. | Agriculture, dairy farming, fishing, forestry, and mining. |

Secondary Sector | Transforms raw materials into finished goods through manufacturing and industrial processing. | Sugar mills converting sugarcane into sugar, car assembly lines, and textile factories turning cotton into clothes. |

Tertiary Sector | Does not produce physical goods; instead, it provides essential services that support the Primary and Secondary sectors. | Transportation (trucks, trains), banking, insurance, education (schools), healthcare (hospitals), and IT services. |

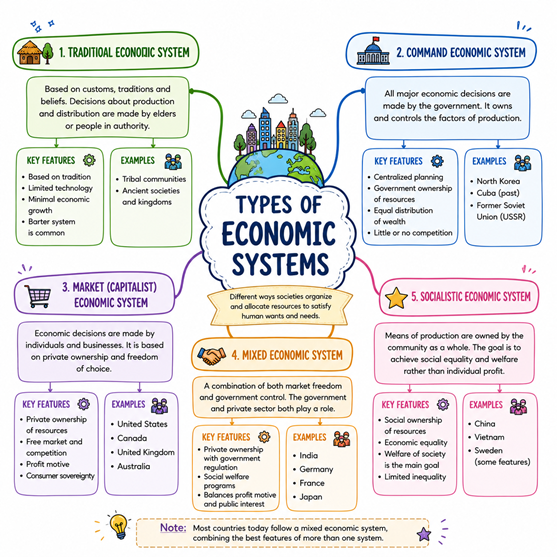

5. Types of Economic Systems

Different countries organize and manage their factors of production through distinct structural frameworks:

1. Capitalist (Market) Economy

- Control: Owned, operated, and managed completely by private individuals or corporations.

- Motive: Driven entirely by the profit motive.

- Price Determination: Prices of goods are decided freely by market forces of demand and supply without government interference (e.g., the United States).

2. Socialist Economy

- Control: Completely owned, operated, and regulated by the central government.

- Motive: Driven by social welfare and the equitable distribution of wealth, rather than individual profit.

- Price Determination: The government decides what to produce, how to produce it, and at what price it should be sold (e.g., historical Soviet Union models).

3. Mixed Economy

- Control: A system where both the private sector and public (government) sector coexist side by side.

- Motive: Combines the efficiency and profit-seeking nature of capitalism with the welfare goals of socialism.

- Example: India. For instance, India has private airlines (like IndiGo) operating alongside government infrastructure, and private schools running alongside government-run public schools.